Accounting Changes and Error Correction Definition

16.05.20

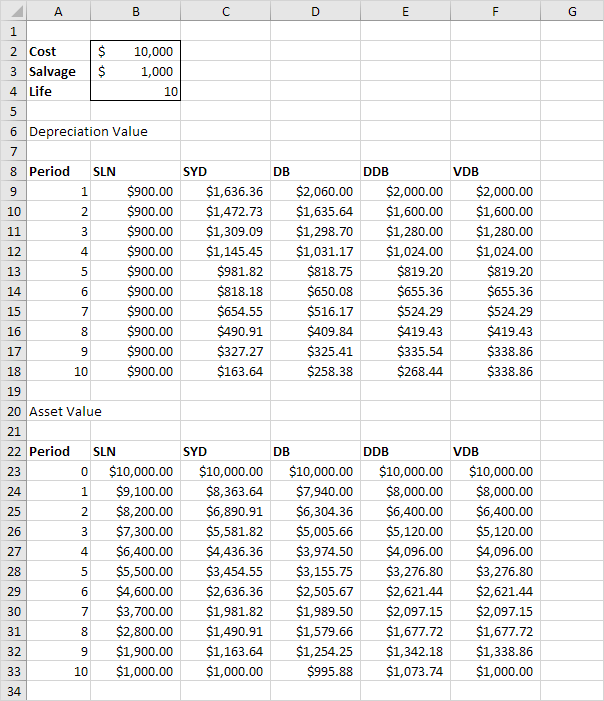

Content

For example, you may enter an invoice as a payment or refund. You will not notice this error in your trial balance because the trial balance will still be in balance.

CPAs rev up for a new tax season – Journal of Accountancy

CPAs rev up for a new tax season.

Posted: Sun, 01 Jan 2023 08:00:00 GMT [source]

Common accounting errors arise from faulty data entry, omission errors, commission errors and errors in principle. In financial statements which reflect both error corrections and reclassifications, clear and transparent disclosure about the nature of each should be included. A trial balance is the sum of credits and debits for all your business’ accounts. If the sum of all your credits and debits for a given account are the same (i.e. balance) then you’re good to go! If they don’t match, it’s time to start reviewing your entries to see if you’ve made one of the errors listed above. The second accounting change, a change in accounting estimate, is a valuation change. This means a material change in estimates is noted in the financial statements and the change is made going forward.

Accounting Errors FAQs

International Financial Reporting Standards are a set of accounting rules currently used by public companies in 166 jurisdictions. The filing of the annual accounts – both the original and the restated accounts – does not of itself imply that such accounts must be presumed to be true or fair. Right now, there’s probably at least one https://online-accounting.net/ area of your business facing transformative change driven by technology or digital risk. Iii.) Trade creditor was overstated for the stationery bought on credit was categorized as goods for re-selling. Liabilities can be classified into two for this purpose, capital and external debts such as non-current and current liabilities.

- For a private company, the correction of a material misstatement is ordinarily accomplished by the company issuing corrected financial statements that indicate that they have been restated and include its auditor’s reissued audit report.

- Some accounting errors can be fixed by simply making or changing an entry.

- A correcting entry in accounting fixes a mistake posted in your books.

A cash sale, $125, had been entered in the sales account as $215. A return of goods to a supplier, Ahmed, $595, had been incorrectly recorded in the purchases returns journal as $295. The sales and purchases account are both understated by $ 1 000. This arises when a transaction is recorded in the wrong personal account.

Detection and Prevention of Accounting Errors

Financial statements of subsequent periods are not required to repeat these disclosures. The quantified materiality of an error must be evaluated with respect to each affected financial statement, as well as each financial statement line item and financial statement disclosure. For example, in addition to considering the income statement, a materiality evaluation under the “rollover” method would also include consideration of the impact on the statement Accounting Errors and Corrections of cash flows. It would also consider whether the cumulative unadjusted errors in the balance sheet result in a material misstatement of the balance sheet or the statement of stockholders’ equity. Under this approach, the entity would correct the error in the current year comparative financial statements by adjusting the prior period information and adding disclosure of the error. A revision disclosure is similar to a restatement disclosure.

What are the 7 types of systematic errors?

- Equipment. Inaccurate equipment such as an poorly calibrated scale.

- Environment. Environmental factors such as temperature variations that cause incorrect readings of the volume of a liquid.

- Processes.

- Calculations.

- Software.

- Data Sources.

- Data Processing.